As a recession looms, interest rates rise, and funding gets harder to acquire, debt financing is becoming a viable alternative SaaS founders and CEOs can use to fuel growth.

This article is part of a three-part series all on raising debt in SaaS—you can check out part one here and part three here.

Let’s dig into the different debt structures and figure out which are the best financing options for your SaaS company.

Understanding debt structures

As you review the different structures, remember that over the last 10 years, only a few SaaS companies and startups repaid their loans with cash from operations. There was always a new round of equity investment or another lender to refinance the debt. That’s much less likely in today’s environment, so structure matters more than ever.

An excellent example of a troublesome structure would be a “bullet loan,” where only interest accrued from the interest rate of the loan is paid until maturity when all the principal is due. This is an excellent structure over the life of the business loan, but you need to be prepared for the financing crisis it will likely create at maturity.

Borrowing under this structure cedes a lot of control to your lender. In fact, several lenders in the market use this structure to acquire SaaS companies under what is known as a “loan to own” model. Default is what the lender hopes to happen, at which time they claim the assets and take over the business.

With structure top of mind and an eye toward cost per month of runway extension, below is a list of the most common debt financing options and structures available from institutional lenders in 2023. The list does not cover debt structures that might be available from angels or financial institutions.

Term Loans

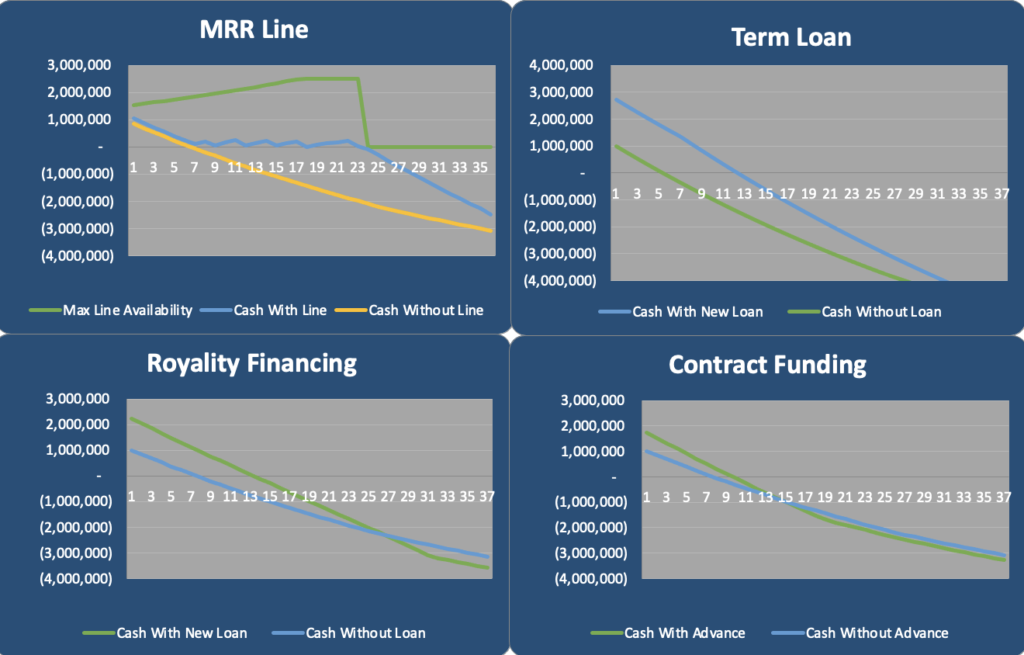

The term loan is still the most common structure in the market today. It is relatively simple to model, and the tradeoffs between costs and runway extension are straightforward.

Keep in mind that altering terms like the length of the interest-only period or the amortization schedule can lower the cost per month of runway extension more than negotiating a lower rate. It’s also the case that the more cash you have in the bank when you draw a term loan, the less it will extend your runway beyond what it would have been otherwise. The SaaS Loan Calculator helps model these tradeoffs.

Financial covenants can significantly shorten the runway extension of a term loan. Balance sheet covenants, in particular, can make some loans useless if the company is required to reserve significant cash balances.

Sometimes term loans can be drawdown in tranches, which generally helps extend the company’s runway and lower overall interest expense. In these cases, be mindful of the conditions that need to be met for future draws and what the lender’s level of discretion is in funding them.

Based on modeling hundreds of actual borrowers, most SaaS companies will be hard-pressed to service debt for a one-time term loan if the amortization period is less than 36 months.

The term loan structure is straightforward to understand, and if the repayment period is long enough, it’s a workable structure for many SaaS companies. Most lenders offer a term-loan structure, including tech-oriented banks and traditional venture debt providers.

Royalty-Based Loans

These loans can be considered term loans where the monthly payment is variable and tied to a percentage of monthly revenue or cash receipts. The advantage of this structure over a traditional bank loan or term loan is that the payments adjust downward automatically if growth or collections slow. In addition, payments automatically change with other cash-flow variability, such as seasonality.

The runway extension characteristics of this structure depend upon the interest payments and repayment rate, which typically goes up over time. In addition, the faster a business grows, the faster it repays the debt, typically up to some predetermined multiple of the original loan.

A sample structure would be a one-time advance of working capital equal to 20% of ARR followed by monthly payments equaling seven percent of monthly revenue in the first 12 months, eight percent in the next 12 months, and nine percent of monthly revenue thereafter until 140% of the borrowed amount is repaid. There is typically also a minimum monthly payment.

Most lenders set the repayment percentages to repay the total amount in 24 to 36 months based on conservative projected revenue growth. This will vary based on your specific repayment terms.

One disadvantage of this structure is that it’s impossible to determine the cost of capital before borrowing the money because repayment is a function of future revenue growth. Because of that, it’s important to model this borrowing to determine the expected cost and runway extension capacity. The SaaS Loan Calculator can help with this.

While challenging to compare to other offerings, the structure may be a good fit for companies whose revenue or cash receipts have significant variability. For example, applications could include usage-based pricing companies or businesses with seasonal historical bookings like ed-tech.

Companies such as Lighter Capital, Element Finance, and dozens of others offer this structure.

MRR-Based Credit Facilities

These are generally constructed as a line of credit you can borrow from as you need, with the maximum borrowing amount tied to a multiple of your company’s MRR. Most facilities are committed for one or two years, and repaid capital can be reborrowed. Some facilities expire with all the principal due then, while others amortize out after the draw period.

If you combine a relatively long draw and repayment period (two and three years, respectively) with an advance rate of five to seven times MRR, this structure provides a meaningful amount of capital over a long period and is effective at runway extension.

In addition, the amount that can be borrowed automatically increases over time as MRR grows.

As with other structures, covenants or a lender’s discretion not to advance funds can diminish the facility’s utility. This structure is also commonly priced to include warrants, making its overall cost higher and difficult to compare to non-dilutive structures.

This is a good structure for most small businesses and growing SaaS companies but does require a fair amount of administration due to the various draws, borrowing-base calculations, and other covenant and financial reporting.

Companies such as SaaS Capital, Bigfoot Capital, and some technology banks offer this structure.

Contract Financing or Subscription Advance Financing

This is what I’m calling the financing provided by firms like Capchase, Pipe, FounderPath, and others. These lenders generally identify specific customer accounts against which to lend and then advance a percentage of the future cash flows expected from those customers.

This approach started as a tactical tool that would advance cash today against a specific monthly payment stream under a longer-term contract vs. a short-term one. Today, however, some companies have disconnected the underlying contracts from the repayments, and the funding structure is more debt-like.

The legal foundation of these arrangements, however, is the sale of current and future accounts receivable related to specific customer accounts. To that degree, these are “factoring” products, and that frame of reference helps understand their costs. In other ways, the structure mimics debt.

Here’s an example structure: a group of your customers has expected payments of $250,000 over the next 18 months. You can sell/borrow against those contracts for 87% of that value today, $217,500, and then repay the $250,000 over the next 18 months. Using the XIIR formula, this is a 19.7% cost of funds.

Importantly, most of these companies establish a “trading limit” for each company, similar to a line of credit amount. The capital provider allows the SaaS company to draw down capital over time up to their trading limit and also to redraw repaid amounts. This “revolving” feature is the most critical component of this structure; without it, the typical individual advance amortization periods are so short, 12 to 24 months, that there is minimal run-way extension capacity.

The drawback to the “trading limit” is that it is reset each month by the lender and is not committed. As a result, it can go up with MRR growth, but it can also go down based on “underwriting” considerations. The specific factors that move the trading limit are not generally disclosed, and the capital provider can set the limit wherever they see fit.

One firm revealed that the primary determinant of setting the trading limit was the SaaS company’s cash runway. In that case, capital availability would disappear just as needed to extend the cash runway, and the company would then be burdened with high debt payments from prior advances.

On the positive side, these new capital providers have raised the bar regarding speed and efficiency. And while it might not be as seamless as the websites suggest, underwriting and funding typically happen in days and weeks, not months, and the transaction costs are virtually zero compared to tens of thousands for a more traditional loan. Moreover, because of this efficiency, this type of capital is available in smaller amounts and to smaller companies than conventional loan products.

It should also be noted that the contract financing companies are willing to advance funds to businesses that already have senior secured lenders. This is because they are actually buying future receivables, and as such, they supersede any lien that might be on the company. And while this approach may be beneficial, entering into such an arrangement is likely a violation of any existing senior loan agreement.

Using the XIRR function and example discount rates from a few different companies, the average cost of funds for this type of product was around 20%.

A final note here on accounting for this type of funding: Most contract finance firms suggest you can book this type of arrangement as debt on your balance sheet and that it has no impact on revenue recognition. However, because these products are so new, different accountants may take different approaches, which you will need to take up with your accountant.

This structure is a good fit if you need capital quickly, you have less than $150,000 in MRR, and you can become comfortable with the discretionary nature of the borrowing limits.

Implications of these debt financing options

Because of the lack of equity dollars in the market today, the role of debt has shifted from dilution avoidance to a breakeven enabler.

CEOs, CFOs, and investors need to carefully consider if using debt to bridge to breakeven will put them in a better or worse position when it comes time for repayment. Generally speaking, higher-growth businesses will benefit from using debt to transition to breakeven at higher MRR levels, while slower-growth companies will not.

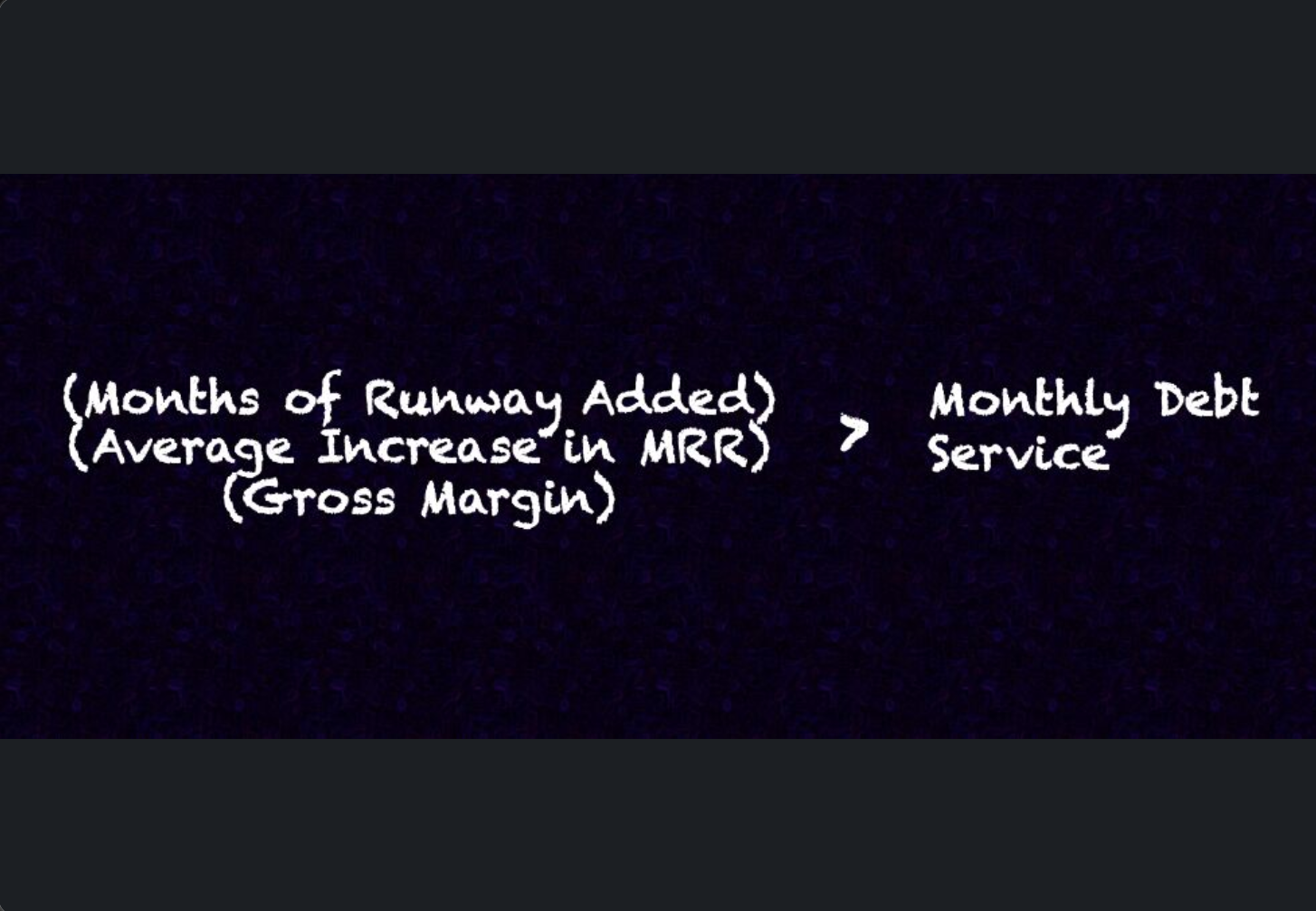

As discussed earlier, the minimum execution level needed for debt to add value is (Incremental MRR*Gross Margin) > (Monthly Debt Service), where incremental MRR is the average monthly growth in MRR times the runway extension period. This is a minimum bar because it assumes the company does not add any other costs to support the new MRR.

On a unit economics basis, you should consider if your CAC payback period is less than the amortization of the loan. In theory, you borrow the money, invest it in a new customer, and then get paid from that customer before you need to repay the loan.

If debt is a good option, structures that deliver the lowest cost per month of runway extension are the least expensive option as long as they don’t create undue financing risk through overleverage, short-payback periods, or future advances subject to lender discretion.

Finding the best debt financing option for your SaaS company

Debt is a tool, and in many ways, it’s more complicated to understand its impact on your business than equity. Once you’ve determined whether or not raising debt makes sense for your company, it can still be difficult to wrap your head around the different kinds of debt structures that are available.

What kind of debt should we take on? Which debt structure will ultimately improve our financial position? How can we model out what cash burn will look like in the months following?

Using this loan analysis calculator, you can determine exactly how much debt you should raise, the debt structure that makes the most sense for your business (line of credit, term loan, revenue-based financing, equity financing, contract funding), and more.

You can access the complete loan analysis calculator here.